Amount of contributions from a citizen of Ukraine who is allowed temporary residence

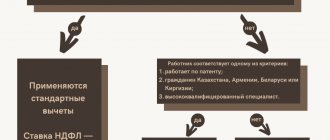

Non-residents pay personal income tax at a 30% rate if their period of residence in the Russian Federation is less than 183 days. But there are a number of foreigners who, not being tax residents, pay personal income tax at special rates:

What is the procedure for calculating insurance premiums and personal income tax from payments under employment contracts in favor of these persons? In accordance with Art. 2 of Federal Law No. 115-FZ of July 25, 2021 “On the legal status of foreign citizens in the Russian Federation” (hereinafter referred to as Law No. 115-FZ), foreign citizens legally staying in the Russian Federation may have the following status: - foreign citizen temporarily staying in the Russian Federation - a person who arrived in the Russian Federation on the basis of a visa or in a manner that does not require a visa, and received a migration card, but does not have a residence permit or temporary residence permit; - a foreign citizen temporarily residing in the Russian Federation - a person who has received a temporary residence permit ;- a foreign citizen permanently residing in the Russian Federation is a person who has received a residence permit. The employer is obliged to make standard transfers according to the established company tariff.

The employee is a citizen of Ukraine: how to pay insurance premiums

In relation to insured persons from among foreign citizens or stateless persons (with the exception of highly qualified specialists in accordance with Law No. 115-FZ) temporarily staying in the territory of the Russian Federation, organizations pay insurance premiums at the rate established by Law No. 167-FZ for citizens of the Russian Federation for financing of the insurance pension, regardless of the year of birth of the specified insured persons (clause 2 of article 22.1 of Law No. 167-FZ).

As we can see, Law No. 125-FZ does not provide for any exceptions for foreign citizens temporarily staying in the Russian Federation. This means that insurance contributions for compulsory social insurance against industrial accidents and occupational diseases should be calculated from the salary of a Ukrainian employee in the generally established manner.

Payment of salary tax to citizens of Ukraine

Good afternoon. Please answer this question for me. I am a citizen of Ukraine. I have been in Russia for 2 months. I applied for temporary asylum and received a certificate of temporary asylum in the Russian Federation. Now I have officially got a job, they told me that they will deduct 30% income tax. I came from Lugansk. Are there any benefits for paying MT for residents of the south-east of Ukraine? Thank you! Lyudmila

For persons recognized as refugees or granted temporary asylum, personal income tax is 13% (Federal Law No. 285 dated October 4, 2021), and also see paragraph 7, paragraph 3, article 224 of the Tax Code of the Russian Federation. Federal Law No. 285 came into force on October 6, 2021, but applies to relationships arising from January 1, 2021. That is, if before October the tax was levied at a rate of 30%, then it is refundable.

We recommend reading: What date of birth allows you to purchase alcohol?

What fees are payable to a citizen of Ukraine who has a residence permit in the Russian Federation?

Contributions to compulsory social insurance are subject to only payments accrued within the framework of labor relations. Social insurance contributions do not need to be assessed for payments under civil contracts for the performance of work or provision of services.

Do not charge compulsory social insurance contributions for payments to foreigners temporarily staying in Russia - highly qualified specialists. An exception is made for highly qualified specialists from EAEU member countries temporarily staying in Russia. They are recognized as insured persons on the basis of existing international treaties, therefore social insurance contributions must be charged at a rate of 2.9 percent for payments in their favor.

Insurance premiums from foreigners in 2021 - 2021

From the income of a foreigner temporarily staying in the Russian Federation who has received refugee status, unlike other foreigners with a temporary stay, additional deductions will be made for compulsory medical insurance using the usual rate for the Russian Federation of 5.1% (letter of the Ministry of Labor of Russia dated February 17, 2021 No. 17-3/OOG- 229).

1. Annual payment for compulsory pension insurance for income not exceeding 300,000 rubles. for the year, will be equal to 29,354 rubles. in 2021. If the income turns out to be more than 300,000 rubles, an additional 1% will be charged on the amount exceeding 300,000 rubles. The total amount of payments cannot be more than 8 times the fixed annual payment 29,354 × 8 = 234,832 rubles. in 2021.

Insurance premiums from citizens of Ukraine in 2021

- the obligation to apply additional tariffs due to the special working conditions of a foreign employee;

- possibility of using reduced tariffs

- Contribution rates for injuries will depend on the type of activity carried out by the employer.

We recommend reading: How to request a certificate from your employer for a pension fund

For temporarily staying foreigners, there are their own rules for transfers, since highly qualified specialists are selected from among them, whose income under any of the contracts is not subject to any contributions, except for injuries. The income of other foreign workers registered under the contract will not be subject to contributions to compulsory health insurance, but will be subject to payments to compulsory health insurance and compulsory health insurance.

How much tax should I pay on the sale of an apartment in Ukraine?

If the object being sold is not registered in the State Register of Rights to Real Estate, when concluding a transaction, the seller is required to obtain a certificate of registration of such an object in the BTI. The standard period for preparing a certificate is 5 working days, the cost is about 600 UAH. However, if you need expedited preparation of a certificate (for example, for an urgent sale), the cost of obtaining a certificate within one day will be about 2,500 UAH. For more information about what the State Register of Rights to Real Estate is, read the article “How to register ownership of real estate.”

Receiving a certificate guarantees the buyer that no one is registered in the apartment at the time of sale. It goes without saying that before the transaction is finalized, all those registered must be written out (unless the parties have agreed otherwise).

We recommend reading: How to write a cheat sheet for traffic rules

Tax from a foreign citizen with a temporary residence permit

Indeed, in accordance with paragraph 1 of Article 226 of the Tax Code of the Russian Federation, employers from whom, or as a result of relations with which the taxpayer received income subject to personal income tax, are recognized as tax agents for the purposes of the Tax Code.

from the implementation of labor activities by participants in the State Program for Assistance to the Voluntary Resettlement to the Russian Federation of compatriots living abroad, as well as members of their families who jointly moved to a permanent place of residence in the Russian Federation, in respect of which the tax rate is set at 13 percent; from the performance of labor activities by foreign citizens or stateless persons, recognized refugees or who have received temporary asylum on the territory of the Russian Federation in accordance with the Federal Law “On Refugees”, in respect of which the tax rate is set at 13 percent.

Lawyer Anna Slobozhaninova answers:

Income in kind, that is, things that also include real estate received from citizens by inheritance, are not subject to income tax for individuals, regardless of their citizenship (Clause 18, Article 217 of the Tax Code of the Russian Federation).

After registering the ownership of the apartment, the heir will be required to pay property tax, starting from the date of state registration of ownership in Rosreestr until the date of registration of the transfer of ownership of the property to another person upon sale. The amount of tax is determined based on the cadastral value of housing. Please note that the cadastral value of real estate may change once a year.

After the sale of an apartment, a foreign citizen pays personal income tax if he is not a tax resident in the Russian Federation. The amount of tax is determined depending on the tax status of the foreign citizen. If a citizen has the status of a tax resident in the Russian Federation, that is, he actually stays on the territory of the Russian Federation for at least 183 calendar days during the year, then the income tax is 13% of the amount received for the sale of the apartment.

The owner of the apartment died. What should the heirs do?

Inheriting an apartment

If the period of stay in Russia is less than 183 days, then the citizen must pay 30% of the cost of the apartment. It should also be taken into account that income received by a foreigner (non-resident or resident) on the territory of the Russian Federation is also subject to taxation in accordance with the legislation of Ukraine. However, in order to avoid double taxation, according to Art. 22 of the Agreement between the Government of the Russian Federation and the Government of Ukraine dated 02/08/1995, in relation to this situation, the rule applies that if a citizen of Ukraine paid tax in Russia, then the amount of tax on income in Ukraine is subject to deduction from the tax paid in Ukraine.

Therefore, in order to sell an apartment in Russia at lower costs, the seller must become a resident of the country, that is, live in Russia for 183 days before concluding a sales contract. It is advisable to sell the apartment three years after receiving the inheritance, and the tax resident status must be maintained during this period. Then you won't have to pay sales tax.

Insurance premiums for foreigners in 2021

Also, from 2021, the provisions of the Treaty on the Eurasian Economic Union came into force, according to which the salaries of foreign workers from the countries of the union (Belarus, Armenia, Kazakhstan, Kyrgyzstan) are subject to contributions at the general rates of insurance premiums, as for employees - citizens of Russia (Article 98 of the Treaty on Eurasian Economic Union dated 05.29.14).

For temporarily staying foreigners, insurance premiums must be paid in 2021 regardless of the duration of the employment contract. This is provided for by paragraph 1 of Article 7 of the Federal Law of December 15, 2001 No. 167-FZ and part 3 of Article 58.2 of the Federal Law of July 24, 2009 No. 212-FZ.

Are insurance premiums calculated from vacation pay - important rules, payment deadlines, examples

Vacation pay is a type of employee income that is the basis for insurance contributions. Contributions are calculated from the calculated amount at current rates and transferred in various payments according to their intended purpose.

If there was a gross error when calculating insurance premiums, then the court will hold the director and chief accountant administratively liable and issue them a fine of 5,000 to 10,000 rubles. When a crime is committed, those responsible may be subject to criminal penalties.

How to levy contributions on remuneration under a GPC agreement with a Ukrainian

This clarification is given by the Ministry of Finance in letter No. 03-15-06/46670 dated July 21, 2021, in which officials answered the question about the calculation of insurance premiums for remuneration to a citizen of Ukraine temporarily staying in the Russian Federation under a civil contract for the provision of services.

In accordance with paragraph 1 of Article 7 of the Federal Law of December 15, 2021 N 167-FZ, insured persons in the OPS system are foreign citizens or stateless persons temporarily residing in the territory of the Russian Federation, working, in particular, under civil law contracts, the subject of which are performance of work and (or) provision of services.

How are Ukrainian citizens taxed?

Relations related to the calculation and payment (transfer) of insurance contributions to the Pension Fund of the Russian Federation for compulsory pension insurance, to the Social Insurance Fund of the Russian Federation for compulsory social insurance in case of temporary disability and in connection with maternity, to the Federal Compulsory Medical Insurance Fund (hereinafter referred to as insurance contributions) are regulated by Federal Law No. 212-FZ of July 24, 2021 (hereinafter referred to as Law No. 212-FZ). According to the provisions of paragraph 15 of the first part of Art. 9 of Law N 212-FZ are not subject to insurance premiums for the amounts of payments and other remuneration under employment contracts and civil law contracts, including under contracts of author's order in favor of foreign citizens and stateless persons temporarily staying in the territory of the Russian Federation, with the exception of cases provided for by federal laws on specific types of compulsory social insurance. 1. Insurance contributions to the Pension Fund of Russia According to paragraph 1 of Art. 7 of the Federal Law of December 15, 2021 N 167-FZ “On Compulsory Pension Insurance in the Russian Federation”, insured persons are citizens of the Russian Federation, foreign citizens or stateless persons permanently or temporarily residing in the territory of the Russian Federation, as well as foreign citizens or stateless persons (for with the exception of highly qualified specialists in accordance with Federal Law dated July 25, 2021 N 115-FZ “On the Legal Status of Foreign Citizens in the Russian Federation”), temporarily staying in the territory of the Russian Federation, who have entered into an employment contract for an indefinite period or a fixed-term employment contract (fixed-term employment contracts) of at least six months in total during the calendar year. From the above norm we can conclude that payments within the framework of labor relations: - with a foreign citizen temporarily staying in the Russian Federation, contributions to the Pension Fund of the Russian Federation are subject to the conclusion of an employment contract for an indefinite period or a fixed-term employment contract lasting at least six months in total during a calendar year ; — foreign citizens temporarily residing in the Russian Federation are subject to contributions to the Pension Fund; — foreign citizens permanently residing in the Russian Federation are subject to contributions to the Pension Fund. 2. Insurance contributions to the Social Insurance Fund According to paragraph 1 of Art. 2 of the Federal Law of December 29, 2021 N 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity” citizens of the Russian Federation, as well as those permanently or temporarily residing in the territory, are subject to compulsory social insurance in case of temporary disability and in connection with maternity Russian Federation foreign citizens and stateless persons. Please note that foreign citizens temporarily staying in the Russian Federation are not listed as insured persons. Thus, from the wording of this norm it follows that payments within the framework of labor relations: - with a foreign citizen temporarily staying in the Russian Federation are not subject to contributions to the Social Insurance Fund; — foreign citizens temporarily residing in the Russian Federation are subject to contributions to the Social Insurance Fund; — foreign citizens permanently residing in the Russian Federation are subject to contributions to the Social Insurance Fund. 3. Insurance contributions to the Compulsory Medical Insurance Fund According to Art. 10 of the Federal Law of November 29, 2021 N 326-FZ “On Compulsory Medical Insurance in the Russian Federation”, insured persons are citizens of the Russian Federation, foreign citizens permanently or temporarily residing in the Russian Federation, stateless persons (with the exception of highly qualified specialists and members of their families in accordance with Federal Law of July 25, 2021 N 115-FZ “On the Legal Status of Foreign Citizens in the Russian Federation”), as well as persons entitled to medical care in accordance with the Federal Law “On Refugees”. Foreign citizens temporarily staying in the Russian Federation are not listed as insured persons. Accordingly, payments within the framework of labor relations: - with a foreign citizen temporarily staying in the Russian Federation are not subject to contributions to the Compulsory Medical Insurance Fund; — foreign citizens temporarily residing in the Russian Federation are subject to contributions to the Compulsory Medical Insurance Fund; — foreign citizens permanently residing in the Russian Federation are subject to contributions to the Compulsory Medical Insurance Fund. 4. Insurance premiums for industrial accidents and occupational diseases In accordance with paragraph 1 of Art. 5 of the Federal Law of July 24, 2021 N 125-FZ “On compulsory social insurance against accidents at work and occupational diseases”, individuals who perform work on the basis of an employment agreement (contract) concluded with the policyholder, as well as individuals performing work on the basis of a civil contract, if in accordance with the specified contract the policyholder is obliged to pay insurance premiums to the insurer. It follows from this norm that foreign citizens working on the basis of an employment contract are subject to social insurance against industrial accidents and occupational diseases (AS and Occupational diseases) on a general basis, since all individuals are insured without exception.

We recommend reading: Commercial proposal for the supply of furniture

In accordance with Art. 2 of Federal Law No. 115-FZ of July 25, 2021 “On the legal status of foreign citizens in the Russian Federation” (hereinafter referred to as Law No. 115-FZ), foreign citizens legally staying in the Russian Federation may have the following status: - foreign citizen temporarily staying in the Russian Federation - a person who arrived in the Russian Federation on the basis of a visa or in a manner that does not require a visa, and received a migration card, but does not have a residence permit or temporary residence permit; - a foreign citizen temporarily residing in the Russian Federation - a person who has received a temporary residence permit; - a foreign citizen permanently residing in the Russian Federation - a person who has received a residence permit.

When a foreigner’s status changes, monthly insurance premiums are calculated at different rates.

When the status of a foreign worker changes during the billing period, insurance premium rates must be differentiated by period: separately for payments for the period when the foreigner was a “temporary resident”, and separately for payments for the period when he became a “temporary resident”. That is, for the month in which the status changed, payments will need to be divided into periods with different statuses and insurance premiums will need to be calculated separately for each part at the appropriate rate.

There are no special norms regulating the procedure for calculating insurance premiums when the status of a foreign citizen changes during the billing period. In this case, one must proceed from the fact that the base for calculating contributions is determined in a general manner on an accrual basis from the beginning of the year. And for the month in which the status changed, payments must be divided into periods with different statuses and insurance premiums must be calculated separately for each part, determining the insurance rate depending on the status of the insured person on a specific date.

Rates for foreign workers

For payments in favor of foreign workers referred to in the commented letter, insurance premiums are calculated as follows:

- payments to temporarily staying foreign citizens - 22% in the Pension Fund of the Russian Federation and 1.8% in the Social Insurance Fund of the Russian Federation (in case of temporary disability and in connection with maternity);

- from payments to temporarily residing foreign citizens - 22% in the Pension Fund, 5.1% in the Federal Compulsory Medical Insurance Fund and 2.9% in the Social Insurance Fund of the Russian Federation (in case of temporary disability and in connection with maternity).

If your foreign employee’s status has changed from a temporary stayer to a temporary resident, tax authorities recommend taking into account the following points:

- apply a different tariff for hospital contributions: 2.9% instead of 1.8%;

- start calculating medical contributions at a rate of 5.1% (they are not charged for payments to temporary residents);

- Determine the contribution base on an accrual basis from the beginning of the year in the same way as for Russian citizens.

In practice, you need to do the following. In the month when the employee’s status changed, divide the amount of payments accrued to him into two parts:

- from the beginning of the month to the day preceding the day on which the employee’s status changed;

- from the day on which the employee’s status changed until the end of the month.

The amount of insurance premiums for the month in which the employee’s status changed is determined using the formula:

Payments to an employee for the period from the beginning of the month to the day of change of status × Rate of insurance premiums until the day of change of status + Payments to an employee for the period from the day of change of status to the end of the current month × Rate of insurance premiums after a change of status = Amount of insurance premiums

New contributions must be paid from payments accrued starting from the day on which the employee’s status changed. How to determine this day?

Date of status change

A foreigner who entered the Russian Federation with or without a visa in cases where the law allows this is considered to be temporarily staying in the country. However, if he plans to stay here for a long time, he has the right to apply for a temporary residence permit (clause 1 of article 2, clause 1 of article 6, clause 1 of article 6.1 of the Federal Law of July 25, 2002 No. 115-FZ.

The date of change of status will be the day the decision is made to issue a temporary residence permit. This will be indicated in the notice that the foreigner receives and in his passport.

The date of change of status is not related to the moment of receipt of documents or presentation of them to the employer.

Example. Calculation of insurance premiums when changing status

On June 17, 2019, employee Sergeev changed the status of a temporary resident to the status of a temporary resident.

For January-May, Sergeev was credited with 300,000 rubles. His salary for June was 60,000 rubles. To calculate insurance premiums for June, the accountant divided Sergeev’s salary into two parts. There are 19 working days in June.

Salary for the period from June 1 to June 16 amounted to 28,421.05 rubles. (RUB 60,000: 19 days x 9 days). Salary for the period from June 17 to June 30 amounted to 31,578.95 rubles. (RUB 60,000: 19 days x 10 days).

As of June 30, the total calculation base for calculating insurance premiums from payments to Sergeev did not exceed the limit values:

- nor for social insurance contributions: RUB 300,000. + 60,000 rub.

- nor for pension insurance contributions: RUB 300,000. + 60,000 rub.

Tariffs for calculating insurance premiums from Sergeev’s salary are:

with temporary residence status:

- for pension insurance – 22%;

- for compulsory social insurance – 1.8%;

- for compulsory health insurance – 0%.

with permanent resident status:

- for pension insurance – 22%;

- for compulsory social insurance – 2.9%;

- for compulsory health insurance – 5.1%.

From payments to Sergeev for January-May, the accountant calculated insurance premiums in the following amounts:

- for pension insurance – 66,000 rubles. (RUB 300,000 × 22%);

- for social insurance – 5400 rubles. (RUB 300,000 × 1.8%);

- for health insurance – 0 rub.

From payments to Sergeev for June, the accountant calculated insurance premiums in the following amounts: for the period from June 1 to June 16:

- for pension insurance – 6,262.63 rubles. (RUB 28,421.05 × 22%);

- for social insurance – 511.58 rubles. (RUB 28,421.05 × 1.8%);

- for health insurance – 0 rub.

for the period from June 17 to June 30:

- for pension insurance – 6947.37 rubles. (RUB 31,578.95 × 22%);

- for social insurance – 915.79 rubles. (RUB 31,578.95 × 2.9%);

- for medical insurance – 1610.53 rubles. (RUB 31,578.95 × 5.1%).

We would like to add that it is in your interests to find out in a timely manner about a change in the status of a foreign worker. If you continue to charge contributions in the old way, at lower rates, it will turn out that you are underestimating the calculation base. And for this your company and manager will be fined.

Migrant Herald

If a foreigner or stateless person temporarily stays

on the territory of the Russian Federation, the employer is obliged to accrue

only pension and social contributions

. Moreover, contributions in case of illness and maternity from payments in favor of such foreigners should be paid at a rate of 1.8%. After all, they are entitled only to temporary disability benefits.

Foreign citizens temporarily staying from countries with a visa-free regime can work in Russia under a patent (Article 13 of Law No. 115-FZ). Accordingly, you need to pay the following insurance premiums for foreigners in 2021 working under a patent:

What is the tax on self-employed citizens in 2021

When registering, a citizen must indicate the region where he operates. If there are several such regions, the self-employed person has the right to choose one of them. At the same time, the place of business can be changed no more than once a year.

According to the new regime, self-employed people will pay tax on income from the sale of goods, works, services, property rights to individuals at a rate of 4%, individual entrepreneurs and legal entities - 6%. Those who switched to it will not pay personal income tax of 13%.

We recommend reading: Does a monthly subscription to the Greater Moscow train cost 1750 or 1950 today?

The salaries of refugees from Ukraine should be subject to contributions similar to the salaries of Russians

According to the current legislation of the Russian Federation, contributions for compulsory pension insurance, compulsory social insurance, compulsory medical insurance are charged on payments to all foreigners who have the status of permanent, temporary residents or temporary residents of Russia (except for temporarily staying highly qualified specialists - contributions do not need to be accrued on their income ). As for citizens of countries that are members of the EAEU (Belarus, Kazakhstan, Armenia), insurance premiums must be paid on payments to them regardless of the migration status of employees, Novichkova recalled.

For payments to foreign employees temporarily staying in Russia (except for highly qualified specialists), contributions to compulsory pension insurance and compulsory social insurance are accrued in the same manner as for the income of Russian citizens.

Contributions to the pension fund

Do not forget that pension contributions that were formed on each person’s personal account can also be checked through the specialized information portal “Gosuslugi”. In addition, it is possible to order the necessary certificate on the official website of the Pension Fund.

- For payments for the formation of the insurance part of the pension - 39210202010061000160.

- For payments to form the funded part of the pension – 39210202020061000160.

- Contributions for compulsory health insurance, which are credited to the FFOMS budget - 39210202100081000160.

- Contributions for compulsory medical insurance, which are credited to the TFOMS budget - 39210202110091000160.

We recommend reading: Total Area of the Apartment and Living Area of the Apartment

Personal income tax and insurance premiums on a foreigner’s income

Unlike personal income tax, for the calculation and calculation of insurance premiums on the income of a foreign employee, the number of days spent in Russia is not important. The most important thing is what migration status the employee has: permanent resident, temporary resident or temporary resident. Let us consider separately the calculation of contributions for each option.

- Tax Code of the Russian Federation

- Labor Code of the Russian Federation

- Federal Law of June 23, 2021 No. 164-FZ “On Amendments to Article 13.2 of the Federal Law “On the Legal Status of Foreign Citizens in the Russian Federation” and Article 1 of the Federal Law “On Amendments to the Federal Law “On the Legal Status of Foreign Citizens in the Russian Federation” Russian Federation"

- Federal Law of July 24, 2021 No. 212-FZ “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund”

- Federal Law of July 25, 2021 No. 115-FZ “On the legal status of foreign citizens in the Russian Federation”

- Federal Law of December 15, 2021 No. 167-FZ “On compulsory pension insurance in the Russian Federation”

- Decree of the Government of the Russian Federation of November 30, 2021 No. 1101 “On the maximum value of the base for calculating insurance contributions to state extra-budgetary funds from January 1, 2021”

- Resolution of the State Council of the Republic of Crimea dated April 11, 2021 No. 2021-6/14 “On approval of the Regulations on the specifics of application of legislation on taxes and fees in the territory of the Republic of Crimea during the transition period”

- Law of the city of Sevastopol dated April 18, 2021 No. 2-ZS “On the specifics of the application of legislation on taxes and fees in the territory of the federal city of Sevastopol during the transition period”

- Letter of the Federal Tax Service of Russia dated July 4, 2021 No. BS-4-11/ “On taxation of income of individuals”

- Letter of the Ministry of Finance of Russia dated October 3, 2021 No. 03-04-05/41061

- Letter of the Ministry of Labor of Russia dated August 29, 2021 No. 17-3/1436

- Letter of the Ministry of Finance of Russia dated June 28, 2021 No. 03-04-06/24677

- Letter of the Federal Tax Service of Russia dated March 5, 2021 No. ED-3-3/ “On the issue of determining the tax status of an individual”

- Letter of the Ministry of Labor of Russia dated February 27, 2021 No. 17-4/342

- Letter of the Ministry of Finance of Russia dated November 15, 2021 No. 03-04-05/6-1301

- Letter of the Ministry of Finance of Russia dated April 5, 2021 No. 03-04-05/6-443

- Letter of the Ministry of Finance of Russia dated February 10, 2021 No. 03-04-06/6-30

- Letter of the Federal Tax Service of Russia dated September 21, 2021 No. ED-4-3/[email protected] “On tax refund”

- Letter of the Federal Tax Service of Russia dated September 5, 2021 No. ED-2-3/[email protected] “On consideration of the appeal”

- Letter of the Federal Tax Service of Russia dated June 9, 2021 No. ED-4-3/9150 “On the procedure for tax refunds to foreign citizens”

- Letter of the Ministry of Finance of Russia dated May 16, 2021 No. 03-04-06/6-108

- Letter of the Ministry of Finance of Russia dated April 28, 2021 No. 03-04-06/6-102

- Letter of the Ministry of Finance of Russia dated April 14, 2021 No. 03-04-05/6-256

- A bill on compulsory social insurance of migrants has been submitted to the State Duma - GARANT.RU, July 29, 2021.

- An entry fee may be introduced for migrants from visa-free countries in Russia - GARANT.RU, June 11, 2021.

Payroll tax rates - table

To support the federal budget, the taxation system of the Russian Federation provides for taxes on real estate, private property, luxury, transport tax and many others. This number also includes personal income tax. What percentage of the salary must be contributed to the state budget? What deductions from wages must be made in addition to personal income tax? These, as well as other aspects of this issue, will be considered in this article.

In addition, so-called injury contributions are made. The interest rate depends on the type of activity of the organization in which the employee is registered. Interest rates for this type of payment are regulated by Federal Law No. 179-FZ of December 22, 2021 and range from 0.2% for the safest types of activities to 8.5% for the most dangerous ones.

We recommend reading: Mortgage in Sberbank Conditions for Large Families

Foreigners who have been granted temporary asylum in the Russian Federation: what about contributions to the FFOMS

If we look at the Law on Compulsory Health Insurance, we will see that those insured in the compulsory medical insurance system include, in particular, persons working under an employment contract who have the right to medical care in accordance with the Law “On Refugees” . In turn, these are:

“Currently, the position of the ministry is that, according to the totality of the norms of the legislation of the Russian Federation, payments and rewards in favor of foreign citizens and stateless persons who have been granted temporary asylum in the Russian Federation are subject to contributions to the Federal Compulsory Medical Insurance Fund in the generally established manner at the rate

Changes to inheritance taxation

Law No. 1910-VIII “On Amendments to the Tax Code of Ukraine regarding the Taxation of Inheritance,” signed on March 24, 2021 by the President of Ukraine, simplifies the registration of inheritance for the testator’s immediate relatives. In accordance with these changes, heirs of the second degree (siblings, grandparents and grandchildren) are exempt from paying personal income tax in the form of 5% of the value of the inheritance. In addition, heirs of the 1st and 2nd degrees of kinship are also exempt from the need to assess inherited heritage objects for tax purposes.

Residents who receive an inheritance abroad are subject to a tax rate of 18%. When determining residence, citizenship does not have primary importance: a resident of Ukraine is a person who stays on its territory for at least 183 days during the year. Even being a citizen of Ukraine, but spending more than 183 days a year outside its borders, the heir is required to pay the maximum tax rate upon entering into an inheritance.

When inheriting property in Ukraine by non-resident persons, the tax rate is also 18%. The estimated tax amount is subject to payment to the state budget. The presence and degree of relationship does not play a role in this case.

For some preferential categories of citizens, taxation is applied at a 0% rate, regardless of their degree of relationship with the testator. This applies to the taxation of inherited movable property and/or real estate (apartment or house), if the heir is:

- disabled person of group I;

- a child deprived of parental care;

- an orphan;

- a disabled child.

However, if the property received by a person belonging to a preferential category is commercial property, as well as in the form of securities, shares, insurance compensation and pension funds from non-state funds, then such inheritance will be taxed at the standard rate.