Labor of foreign citizens in Russia (residents and non-residents)

Within the framework of the country's tax code, a tax resident is a person who has stayed within the territorial borders of the state for at least 183 days during the last year. Acquiring this status obliges a person to transfer to budget funds amounts equivalent to the amount of taxes levied on Russians. Consequently, from a legal point of view, non-residents and persons residing in the Russian Federation on a temporary basis are equal in tax obligations.

Personal income tax for foreign citizens in 2021

In accordance with the Tax Code of the Russian Federation, tax residents include people who have been on its territory for more than 183 days over the past 12 months. If a foreigner has received this status, then taxes are withheld from him in the same amounts as from Russian citizens. Thus, personal income tax from a temporarily residing foreigner in 2021 is withheld in the same way as from a non-resident.

Personal income tax from a foreigner working under a patent is withheld as follows: first, after the patent is issued, the employee pays a fixed advance, then the employer obtains a certificate from the fiscal authority confirming the possibility of reducing the tax by the amount of the advance paid. After confirmation - this takes no more than 10 days - the accountant who calculates the foreigner’s salary can safely reduce the amount of payment to the budget by the amount of the advance.

We recommend reading: How long will private kindergartens receive subsidies?

Employment contract with a foreign specialist

Legal confirmation of legal work activity is a contract. Moreover, every foreigner has the right to demand from the employer that the contract does not have a time frame, despite the fact that migration structures believe that as soon as the validity period of the patent can be considered expired, the contract will also lose its legal force.

Reference! The Labor Code of the Russian Federation regulates only the temporary removal of an employee from a position until the documents are extended and put in order.

Personal income tax of a citizen of Tajikistan in 2021

The official employment of any professional can only be confirmed by signing a written employment contract. The method of consolidating relations with foreigners was no exception in this regard. Moreover, the Labor Code (LC) of the Russian Federation guarantees to all categories of visiting specialists that they can demand that the employer enter into a contract without limiting the duration of its validity. And although migration services insist that upon expiration of a work permit or patent, the contract loses its force, labor legislation only provides for suspension from work for the period of renewal or re-issuance of documents.

Details of the issuance of work visas, permits and patents, as well as a list of categories exempt from issuing any permits, are discussed in the topic on the labor activity of foreign citizens in the Russian Federation. Naturally, a future employer has the right, and sometimes the obligation, to require a larger number of papers for subsequent employment from a person who has arrived from another country. These, in particular, include a mandatory VHI policy, a work patent, and a migration registration document. The flow of labor migrants to Russia is quite large and annually brings a considerable share of taxes and fees to the budget. Today you can meet a foreigner at almost any enterprise and in any field. The income of each of them is also subject to taxation and, unlike citizens permanently residing in Russia, the personal income tax of foreign workers in 2021, as in previous years, is calculated according to different rules.

We recommend reading: Didn’t work due to family reasons

Personal income tax rate for foreigners

The total amount of bets on earned funds is equivalent to 30%. This is according to the law. But in practice everything is somewhat different:

- 13% is transferred from total income;

- certain categories of persons will contribute the same amount to the budget from their salaries, and an additional 15% from their dividends and compensations;

- if a person is the founder of a business company in Russia, then his dividends will be reduced by 15%, and other income items will be reduced by 30%.

Note! If within 12 months a person, due to current circumstances, changes his status and is no longer a resident, then his PFDL will be considered under a preferential scheme.

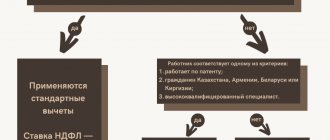

If the payer works on the basis of temporary residence permit

The regulations do not contain clear recommendations in this regard. It is recommended to apply general rules and refer to the rate specified in Article 224 of the Tax Code - standard tax of 13%. For employees working for a temporary residence permit, the calculation system should be used, as for other Russian citizens.

Highly qualified specialists

This concept is determined by the level of the employee’s monthly income. He can be considered highly qualified if a person earns at least 85 thousand rubles per month. 13% tax deductions will be deducted from his total profit. Moreover, if he is entitled to compensation, he must pay 30% of it.

Citizens of EAEU member countries

People who have citizenship of states that are permanent members of the economic Eurasian Union are protected by international treaties, within the framework of which they cannot be deducted from them into the tax budget an amount greater than what citizens of the Russian Federation pay. Therefore, it is the same 13%.

Amount of deductions from the salaries of persons with a patent

Those who carry out their labor activities under a patent transfer tax fees as follows. Once the patent is issued, an advance payment must be made. This value is fixed. Then you need to contact the fiscal authorities and obtain permission from them to change the advance tax assessment downward. The law allows no more than 10 days to make such a decision, after which the amount of contributions to the budget will be reduced by exactly the amount of the advance already made.

This video describes in detail how personal income tax is calculated for persons working under a patent:

How much will a non-resident give to the budget?

A foreigner with a visa will be able to work in the Russian Federation only with permission, and at the same time he will lose 30% of his income every month until the threshold of his stay in the country exceeds 183 days. The reduction rate works only for beneficiaries and persons with special status.

Personal income tax for non-resident shift workers

Working on a rotational basis does not reset the period during which the foreigner lived in the Russian Federation. At the same time, for the period when he is outside the state, the countdown will be automatically suspended. After the required number of days is calculated, the rate will be changed from 30% to the standard 13%.

Income tax for refugees

A person can consider himself a refugee only if he has official confirmation of this. This is proven by a special document, which states that he was forced to move by an emergency situation in his homeland. The migrant’s income will also be deducted 13%.

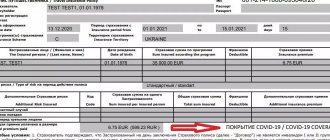

Personal income tax on interest on deposits

Tax is imposed on the total interest income on deposits (account balances) in Russian banks paid to an individual for a calendar year, minus non-taxable interest income.

Non-taxable interest income is calculated as follows:

1 million rub. x key rate of the Central Bank of the Russian Federation on the 1st day of the tax period.

Interest income on foreign currency accounts and deposits is recalculated into rubles at the Central Bank exchange rate in effect on the date of actual receipt of such income.

Please note: when determining the tax base, the following income is not taken into account:

- in the form of interest on ruble deposits, the interest rate on which during the entire tax period does not exceed 1% per annum;

- on escrow accounts (property set aside to fulfill another obligation).

So, when calculating tax:

- take into account all the citizen’s deposits and accounts opened in banks;

- deduction in the amount of interest accrued at the key rate of the Central Bank for 1 million rubles.

This is established by Article 214.2 of the Tax Code of the Russian Federation and has been applied since 2021 (Federal Law No. 102-FZ dated April 1, 2020).

Thus, having received taxable income in the form of bank interest on their deposits in 2021, a citizen must transfer 13% of personal income tax from them to the budget no later than December 1, 2022.

Calculation example

Let's look at a specific example of how the system for calculating personal income tax with foreign citizens works. Let’s say a person transfers 1,000 rubles every month as an advance payment, and this amount is fixed and adjusted by regional coefficients, the value of which may change.

This year it amounted to 2.319, while the deflator for the same period of time stopped at 1.623.

Based on these values, a foreign citizen must pay:

1,000 x 2.319 x 1.623 = 3,763.74 rubles.

KBK

BCCs for foreign migrants are assigned taking into account the following categories:

- from profit;

- patent work;

- when calculating the rate at 13%

- at a rate of 30%;

- in order to avoid double taxation at non-resident rates.

From this video you will learn how personal income tax is correctly calculated and withheld from foreign citizens who work in the Russian Federation:

Compensation payments

This category includes incentive income accruals. They are an integral part of earnings and cannot be separated from it when calculating the amount that must be transferred as a tax deduction.

It should be understood that compensation cannot be remuneration for conscientious work and is therefore taxed at the highest rate.

Hiring a citizen of Ukraine in 2021

- When inviting patent applicants to work, the employer is first of all obliged to verify the availability of an issued patent, as well as the compliance of the positions or area of work specified in the patent with the vacancy. In addition, a patent is issued and is valid exclusively on the territory of one subject of the Russian Federation, and if it is necessary to change the position of an employee or move to the territory of another part of the country, it is also necessary to replace the patent.

- In addition to the patent itself, the employer is also obliged to check that the applicant has a migration card and documents confirming the availability of medical insurance or medical support from an accredited medical institution. It is prohibited to employ Ukrainians who do not have a residence permit or temporary residence permit without insurance.

We recommend reading: From what funds is maternity capital paid?

Many employers, accountants and HR specialists are interested in how the hiring of a citizen of Ukraine should be carried out in 2021. Considering the high level of employer responsibility for violation of labor and migration laws, any mistake can become critical for the enterprise. It should be understood that the procedure for hiring Ukrainians with a temporary residence permit (temporary residence permit), refugees and migrants, with a residence permit or patent is different, which should also be taken into account by the person responsible for personnel appointments.

How to return overpaid personal income tax

The first thing you need to do is prepare a package of documents. There are no clear requirements in this regard; everything is considered individually. In this case, all copies of payment documents are submitted in full. A person should understand that fees must be transferred to the tax office where the employer’s enterprise is registered.

The migrant submits a personal petition with a request to return the overpaid funds for the past reporting period. Tax officials will study the document and make a decision.

Refugees from Ukraine: hiring, personal income tax, contributions and benefits

— maternity benefit; — a one-time benefit for women registered in medical institutions in the early stages of pregnancy; — one-time benefit for the birth of a child; — monthly child care allowance, etc.

Since Ukrainian refugees and Ukrainians who have received temporary asylum can be hired without permits, it turns out that in terms of employment they are practically equal to Russians (subclauses 11 and 12 of clause 4 of article 13 of Law No. 115-FZ). Consequently, there is no need to notify the employment service and the territorial branch of the Federal Migration Service of Russia about the conclusion and termination of labor relations with them (clause 9 of Article 13.1 of Law No. 115-FZ).

We recommend reading: How to get into Eaglet through a portfolio Rostov region